This post contains affiliate links. If you purchase through our links, we may earn a commission at no extra cost to you.

Most digital nomads buy the wrong insurance because they are solving the wrong problem.

They search for “best insurance,” then compare one travel-insurance product against one international-health product as if those were interchangeable. They are not. One is usually trying to protect a trip. The other is trying to protect a person living abroad.

That distinction is what decides whether SafetyWing, World Nomads, or Cigna Global makes sense.

Travel insurance vs international health insurance:

This is the first split to get right.

Travel insurance is built around unexpected problems on a trip:

- emergency medical events

- cancellation or interruption

- evacuation

- delayed or lost baggage

- gear loss, depending on the policy

International health insurance is closer to ongoing medical cover for people living abroad longer term.

That is why the products feel so different on their own sites:

- SafetyWing markets nomad-focused coverage with renewable plans and two layers: Essential and Complete.

- World Nomads frames its product around trip protection, emergency medical events, gear, and annual or single-trip plans.

- Cigna Global markets full international health plans for globally mobile professionals, families, and long-term overseas residents.

If you get this first question wrong, the rest of the comparison becomes noise.

SafetyWing vs World Nomads vs Cigna Global

Here is the practical version.

| Option | Program | Core requirement | Approx. threshold / best fit | Note | Source |

|---|---|---|---|---|---|

| SafetyWing | Nomad Insurance Essential / Complete | Travel medical coverage with nomad-oriented recurring plans and optional fuller health cover | Best fit: long-term solo nomads and lighter long-stay setups | Strong mobility fit, weaker than full expat plans for every family or chronic-care case | Official |

| World Nomads | Travel insurance | Emergency medical cover plus trip-protection logic for active travel | Best fit: frequent trip-based travelers | Stronger on baggage, disruption, and adventure framing than on ongoing health-system replacement | Official |

| Cigna Global | International health insurance | Configurable global medical plans for people living abroad longer term | Best fit: expats, families, and serious long-stay movers | Broader medical framing, but usually pricier and heavier than a lightweight nomad needs | Official |

That table is more useful than star ratings because it matches the purchase to the job.

SafetyWing: why it keeps becoming the default nomad choice

SafetyWing wins a lot of digital nomad comparisons because it speaks the language remote workers actually use.

Its current official positioning is straightforward:

- coverage across 180+ countries

- ability to buy while abroad

- recurring pricing logic

- an Essential plan and a more comprehensive Complete plan

The current public pricing page also makes the split clear. SafetyWing’s site describes Essential as travel medical insurance and Complete as fuller health insurance with extra travel protections.

That is why SafetyWing is often the easiest answer for solo nomads who are not trying to recreate a full domestic insurance system. It is built for mobility first.

The catch is just as important: if your real need is broad ongoing care, family coverage, or a long-term residence setup that behaves more like traditional health insurance, SafetyWing may not be the final answer.

World Nomads: best when the trip itself still matters

World Nomads is still one of the clearest trip-protection products for people who travel often and want the insurance to look and feel like travel insurance.

The company’s own digital nomad page emphasizes:

- emergency medical expenses

- trip cancellation, delay, and interruption

- emergency evacuation

- baggage and personal-tech coverage

- annual or single-trip plan logic depending on market

World Nomads also explicitly says its digital nomad travel insurance is not the same as everyday or preventive healthcare.

That is the key filter.

World Nomads makes the most sense if your bigger fear is a disrupted trip, stolen gear, or emergency event during active travel. It makes less sense if you are trying to solve “I need something that functions like my ongoing health system while I live abroad for a year.”

Cigna Global: expensive, but solving a different problem

Cigna Global is rarely the cheapest answer, and that is exactly why it belongs in the comparison.

It is not really competing to be a scrappy nomad add-on. Cigna positions itself as international health insurance for globally mobile professionals, families, and people living or working abroad longer term. Its own site emphasizes:

- international health plans

- broad provider networks

- support in 200+ markets and territories

- multilingual support

- configurable global medical cover

That is a very different purchase from “I need coverage while I bounce between countries for the next six months.”

So yes, [Cigna] can look like overkill in nomad comparisons. For a lot of solo remote workers, it is. For a family relocating under a long-stay visa, it may be the first product in this comparison that is actually shaped like the problem they have.

Which one fits short trips, long stays, and families?

Use this simple split.

Choose SafetyWing if:

- you are a solo nomad or couple

- you want something built around mobility

- you want a simpler recurring payment model

Choose World Nomads if:

- your trip protection matters as much as your emergency medical cover

- you care about baggage, delays, and active-travel style risks

- your travel pattern is still very trip-shaped

Choose Cigna Global if:

- you are planning a long stay abroad

- you want something closer to full international health insurance

- you are covering a family or want deeper medical structure

This is also where the visa angle starts to matter. If you are comparing countries, the best digital nomad visas in 2026 is the useful next step because insurance requirements vary enough that the country choice can change the insurance answer.

Spain is a good example of that mismatch because the Spain visa paperwork discussion quickly turns into document quality and coverage scope, not just price.

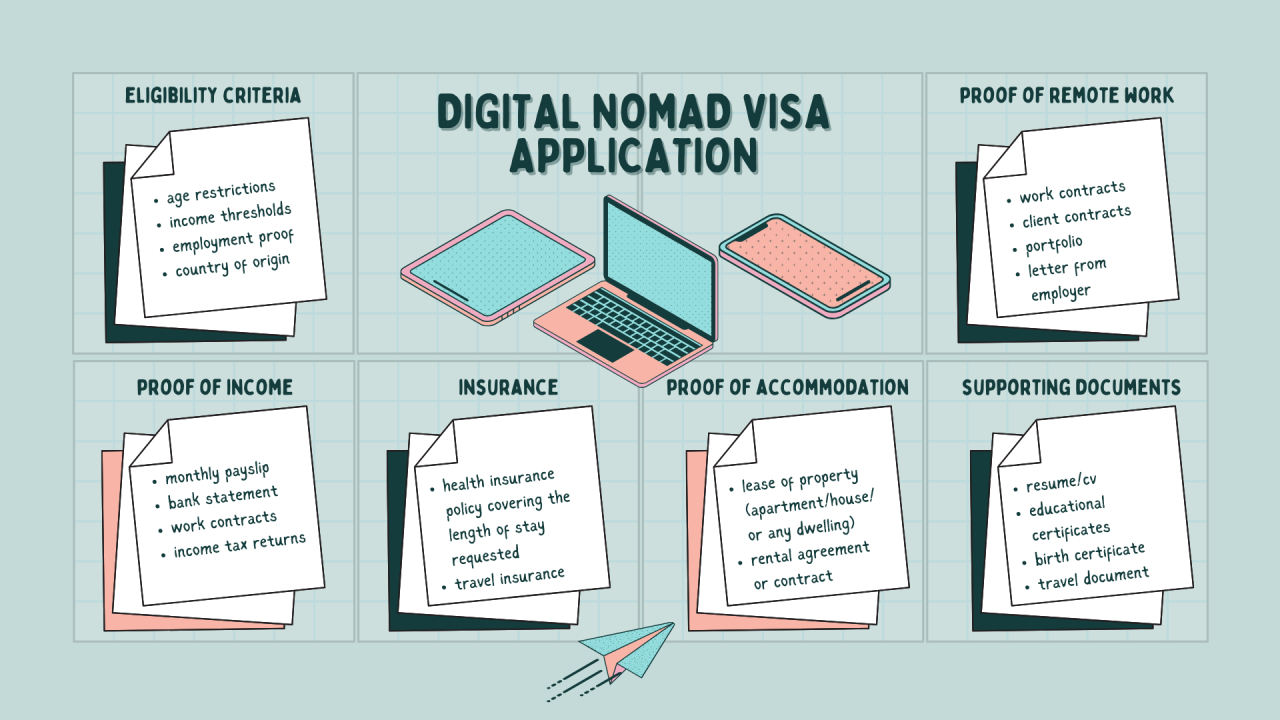

What digital nomad visas usually require from insurance

Many nomad visas require some kind of health or travel insurance, but the exact requirement changes by country.

That means you should stop asking “Which insurer is best?” in the abstract and start asking:

- does the country want travel insurance or fuller health insurance?

- does the country require a coverage minimum?

- does the policy need to cover the whole intended stay?

- are evacuation, hospitalization, or repatriation explicitly referenced?

This is where people waste money. They buy an insurance product that is fine in general and wrong for the visa file.

Portugal creates the same problem, which is why the Portugal D8 breakdown is worth reading before you buy a cheap policy that looks fine and proves nothing.

The exclusions that matter before you buy

The biggest insurance mistake is buying off the headline and ignoring the exclusions.

Three things matter more than most readers expect:

- whether the product covers emergency-only events versus broader ongoing care

- whether professional gear, laptops, or work equipment are covered or limited

- whether the plan works cleanly if you are already abroad when you buy

Those are not side questions. They are the product.

Croatia is the cleaner example here: Croatia’s digital nomad route is easier to plan when the insurance, funds, and stay length all line up from day one.

What to check before you buy any policy for a visa application

This is the part people rush because insurance feels like the least interesting part of the file.

It is not.

If the visa route expects coverage for the full stay, emergency treatment, hospitalization, or repatriation, you need to match the policy wording to the immigration requirement instead of assuming “international” means “acceptable.” That is where cheap travel insurance purchases go wrong. The product may be legitimate. It may simply be the wrong product for the visa standard you need to satisfy.

A cleaner way to review any policy is to check it against four practical questions:

- does it cover the whole period you intend to stay?

- does it behave like trip protection or like ongoing medical cover?

- are there exclusions that make the policy weak if you are already abroad?

- can you produce a certificate or wording summary that a consulate can actually read?

That last point sounds boring. It saves a lot of wasted money. A policy that works in real life but creates confusion on paper can still slow the application down.

And yes, this is where digital nomads keep buying on brand. The brand matters less than the fit.